While digging into Spotify’s annual usage stats, one number stopped me in my tracks: Spotify now drives nearly 13% of global internet traffic and serves over 713 million users worldwide. Crazy, right? I couldn’t just scroll past, I had questions, and I bet you do too:

- Who founded Spotify, and why?

- Where did the idea come from?

- Why did it take off so fast?

- What made it different from everything before it?

Chasing these answers sent me down a rabbit hole of reports, interviews, and industry data. And here’s the kicker. I uncovered some stories that most people don’t know.

So, I decided to document it all for you. Not a dry timeline, but a story that’s insightful, entertaining, and full of lessons, whether you’re a music lover, a marketer, or just curious how one platform shook the entire industry.

Let’s dive in and explore Spotify’s journey together.

The Struggle for Music: Years That Changed Everything (1999–2008)

According to Wikipedia, the early days of digital music (roughly 1998–2001) set the stage for a massive shakeup. Peer-to-peer networks like Napster and Kazaa suddenly made music instantly accessible, and legal buying? Almost irrelevant. (IFPI Music Report)

One click. One file.

Instant access. No checkout.

No waiting. No friction.

The industry was blindsided. Until platforms like Spotify appeared in 2008, the music world was fighting fires on all fronts. Let’s rewind and see how it all unfolded:

Music Industry & Piracy Timeline (1998–2008)

1998 — RIAA Begins Legal Action Against Online Music Sharing

The Recording Industry Association of America (RIAA) takes aim at unauthorized music sites, marking the start of formal battles against digital piracy. (Wikipedia)

1999 — Napster Launches and Changes Music Access Forever

Napster lets users directly share MP3 files. Suddenly, music is everywhere, anytime. (Pew Research Center)

2000 — Metallica Sues Napster

In 2000, the music industry faced a high-stakes showdown when artists decided to fight back. Metallica, along with several other prominent musicians, filed a lawsuit against Napster for copyright infringement. According to industry reports, this case didn’t just target the platform—it ignited a massive public debate about digital piracy, artists’ rights, and the future of music distribution. For the first time, the world saw just how disruptive peer-to-peer sharing had become, and how far the industry would go to protect its content.

1999–2001 — Napster Faces Lawsuits and Shuts Down

Record labels sue Napster for copyright infringement; in 2001, a court orders Napster to stop allowing users to share copyrighted files, leading to its shutdown. (Wikipedia)

2001–2002 — New p2p Networks Emerge

Decentralized programs like Kazaa, Morpheus, LimeWire, and WinMX explode in popularity, harder to control legally and technologically. (users.wfu.edu)

2003 — RIAA Sues Individual Downloaders

The recording industry shifts strategy and starts legal action not just against platforms but against tens of thousands of individuals who shared music files, leading to widespread fear and controversy. (Electronic Frontier Foundation)

2003 — Itunes Music Store Launches a Legal Alternative

Apple launches iTunes, selling digital tracks for $0.99 each and creating one of the first successful legal music marketplaces that actually turned piracy users into paying customers.

2005 — Supreme Court Ruling in MGM v. Grokster

The U.S. Supreme Court rules that companies distributing software that promotes copyright infringement can be held liable, significantly impacting file‑sharing networks. (City Research Online)

2006–2007 — P2p Piracy Remains Widespread; CD Sales Collapse

Despite legal pressure, P2P file sharing continues to thrive, and global physical music revenue keeps falling sharply as consumers shift habits. (Wikipedia)

2008 — Industry Abandons Mass Lawsuits, Piracy Still Entrenched

After thousands of lawsuits, the RIAA steps back, seeking new tactics. Meanwhile, decentralized sharing grows stronger, setting the stage for a new kind of music platform. (Wikipedia)

Chapter 1

The Problem Spotify Was Actually Built to Solve

This section focuses on the real problem Spotify was built to address: how people actually access and consume music over time.

I’ll walk you through what users wanted, how their behaviour changed, and why those shifts made Spotify’s model inevitable earl on.

Spotify was founded in April 2006 in Stockholm by Daniel Ek and Martin Lorentzon, at a time when Napster had collapsed and Kazaa dominated illegal music distribution. Ek argued publicly that piracy could not be solved through legislation alone and that only a faster, superior service that compensated rights holders could change user behaviour. When Spotify launched in October 2008, the music industry was in crisis not because audiences stopped loving music, but because how people accessed it had fundamentally changed. This was the environment Ek and Lorentzon were observing and responding to.

Before diving deeper into the industry collapse, it’s worth grounding Spotify as a company.

| Category | Details |

|---|---|

| Company Name | Spotify Technology S.A. |

| Business Model | Publicly listed company |

| Stock Listing | NYSE (Ticker: SPOT), part of the Russell 1000 Index |

| Year Founded | 2006 |

| Founding Month | April |

| Founding Location | Sweden |

| Registered Office | Luxembourg |

| Operational Headquarters | Stockholm, Sweden |

| Global Presence | 15 offices worldwide |

| Markets Served | Global audience (with limited country restrictions) |

| Core Industries | Music streaming, audio streaming, podcasting |

| Founders | Daniel Ek, Martin Lorentzon |

| Leadership | Daniel Ek (Chairman), Alex Norström (Co-CEO), Gustav Söderström (Co-CEO) |

| Major Subsidiaries | Spotify AB, Spotify USA Inc., Spotify Ltd (UK), plus regional entities |

| Employees | 7,323 employees (as of September 2025) |

| Official Website | spotify.com |

| Account Requirement | User registration required |

| Launch Date | 7 October 2008 |

| Years Active | 17+ years |

At the turn of the millennium, physical recorded music was at its peak. In 1999, global revenue from physical music products hit about $37 billion (NBER Conference), but by 2007, it had fallen to roughly $25 billion, a 32% drop in under a decade. In the U.S., the decline was even steeper: from $12.8 billion in 1999 to $5.5 billion in 2008 (National Bureau of Economic Research), even after counting digital sales. The collapse wasn’t gradual; it was structural.

Why the collapse? Piracy had gone mainstream. Napster’s 1999 launch made it possible to get any song with one click, for free (Pew Research Center). By 2000, a quarter of all adult internet users were downloading music online, over half using Napster. This wasn’t fringe behaviour; it was becoming normal internet usage. The industry responded aggressively: the RIAA sued Napster in December 1999 (WIRED). Napster eventually shut down in 2001, but the peer-to-peer model had already spread to Kazaa, LimeWire, and BitTorrent (EBSCO).

Even after lawsuits against 30,000 individual downloaders between 2003–2006 (WIRED), piracy didn’t stop. Users had already shifted: they wanted instant access, massive catalogs, and zero friction (Wikipedia). Price wasn’t the issue anymore; convenience was king. Once that expectation was set, there was no returning to ownership-first models.

Spotify’s founders, Daniel Ek and Martin Lorentzon, understood this. They weren’t building another music store. They were solving a problem set by piracy:

- Streaming instead of downloads

- Instant search and playback

- A massive catalog with no ownership hassle

These ideas would later define not just Spotify’s product, but the future of music consumption itself.

Their approach worked. In Sweden, where Spotify first launched, illegal downloads dropped by roughly 25% as users adopted the legal alternative (swedishwire.com). It wasn’t a complete solution yet, but it proved that user behaviour could be changed when convenience finally aligned with legality.

Chapter 2

Licensing Before Launch — The Hardest Part Nobody Talks About

This section dives into the behind-the-scenes reality of launching Spotify before it ever went live.

I’ll break down why licensing was the biggest obstacle, how labels reacted, and what Spotify had to negotiate just to legally exist.

Spotify’s success wasn’t just about building a slick app. The real magic happened behind the scenes, in the negotiation rooms with the world’s most powerful music companies, long before the public ever saw a single feature. Most popular histories focus on product design and growth metrics, but licensing rarely gets the same attention because it unfolds slowly, privately, and through legal frameworks rather than headlines. Yet the early licensing deals were extensive, unprecedented, and critical to Spotify’s rise.

Delayed Launch: Licensing Before Users

Spotify was founded in 2006 by Daniel Ek and Martin Lorentzon. But it didn’t launch publicly until October 2008, nearly two and a half years later. This wasn’t about polishing the product; it was about securing legal rights to stream millions of songs across Europe (Scribd). Unlike many tech startups that launch early and iterate later, Spotify couldn’t afford to release a product without label approval. Doing so would have been illegal from day one. From the outset, Spotify was constrained not by technology, but by contracts.

Negotiations dragged on because labels weren’t merely slow or bureaucratic. They were deeply unconvinced that streaming could generate sustainable revenue at all. Years of piracy had trained the industry to see digital distribution as a threat rather than an opportunity, making every agreement unusually cautious and complex.

Even Daniel shared how hard this part was for them in a podcast with This Week in Startups.

Equity for Access: Major Labels Took a Stake

In mid-2008, Spotify offered labels equity instead of, or in addition to, large upfront payments. According to the UK Parliamentary inquiry, music rights holders were granted a combined 18% equity stake at launch:

- Sony BMG: ~6%

- Universal (including EMI): ~7%

- Warner Music Group: ~4%

- Merlin (independent labels): ~1%

This allocation meant labels weren’t just licensing content. They became co-owners of the business. This structure fundamentally changed the dynamic of the negotiations. Corporate filings confirm the very low nominal price paid by the labels for these shares (~€8,804 total) (Music Business Worldwide).

Why Equity, Not Cash, Changed the Game

Labels were skeptical of streaming. They feared revenue loss from piracy, had limited experience with subscriptions, and were still selling downloads. By giving them skin in the game, Spotify aligned incentives: if the company succeeded, the labels profited. At the time, this approach was highly unconventional, especially for a startup with no proven user base. Licensing was no longer a short-term transaction; it became a long-term partnership.

Revenue Shares & Long-Term Payouts

Even with equity, labels insisted on high revenue shares. Early reports and academic analyses show that rights holders received most of the revenue long before Spotify became profitable (Georgetown Law). These deals defined Spotify’s financial structure from day one and made profitability secondary to establishing trust and access. The economic trade-off was clear: scale first, margins later.

Why Labels Trusted Spotify More Than Apple or Google

Spotify’s model won over labels for three key reasons:

- It didn’t threaten existing digital downloads like Apple’s iTunes.

- It offered detailed reporting on user behavior, something file sales never did.

- Equity stakes aligned long-term incentives, a feature absent from other tech companies.

Unlike Apple or Google, Spotify had no hardware ecosystem or operating system to protect, making it appear less structurally threatening to the industry. By the time Spotify went public in April 2018, even after dilution, Sony still held around 5.7% of the company (CNBC). These early deals not only secured content. They shaped Spotify’s operating margins and shareholder composition long before the first million users joined.

Chapter 3

The Freemium Gamble That Nearly Broke the Company

This section explores why giving music away for free was such a risky move for Spotify.

I’ll break down how the freemium model worked, why it worried labels and investors, and how it nearly pushed the company to the edge before it paid off.

When Spotify launched publicly in October 2008, it did so with a strategy that most of the music industry considered dangerously unconventional: give music away for free. At a time when labels were desperate to earn any revenue from digital music, Spotify bet its entire future on a model that initially made no money from most of its users. That model was the freemium approach, and it almost didn’t pay off. In fact, for several years, it looked like a deliberate decision to lose money at scale.

Early Financial Realities — Losses and Cost Structure

Right after launch, the numbers told a stark story. In 2008, Spotify posted a loss of SEK 31.8 million (~$4.4 million USD) (Wikipedia), and by 2011, net losses reached nearly $60 million on revenues of $244 million, with 2012 projected to see another $40 million loss on $500 million revenue. Growth was accelerating, but profitability remained distant.

Why so high? Every stream generated royalty obligations, whether the user paid or not. About 70% of revenue went straight to rights holders. Free users were far from cheap. Spotify was effectively paying licensing costs upfront in exchange for future user loyalty.

Ad-Supported Streaming — A Loss Leader

Spotify balanced two revenue streams:

- Premium subscriptions — the eventual core engine of profitability.

- Ad-supported free tier — initially designed as a funnel rather than a profit center

In the early years, advertising revenue was small and often insufficient to cover royalty costs. Even much later, the imbalance remained visible: in 2023, ad-supported revenue reached €1.68 billion, compared to €11.56 billion from premium subscriptions (FourWeekMBA). This contrast highlights how long Spotify tolerated losses on free users to protect growth.

The freemium model required careful balance. Ad revenue plus subscriptions had to subsidize millions of free listeners, a high-risk proposition in the early 2010s when streaming economics were still unproven.

Freemium Conversion Psychology — The Core Strategic Insight

Spotify’s freemium model wasn’t just free music; it was a behavioral masterstroke.

- Habit Formation and Loss Aversion: Users experienced immediate value and built daily listening routines. Over time, losing access to playlists, recommendations, and uninterrupted playback felt like giving something up rather than gaining something new.

- Investment Increases Switching Costs: Playlists, saved libraries, and personalized recommendations anchored users emotionally and behaviorally. The more time users invested, the harder it became to leave.

Essentially, Spotify turned free engagement into paying behavior not by coercion, but by designing a service users found difficult to abandon.

Why Spotify Refused to Remove Free Access

Labels initially assumed legal alternatives had to be paid. Spotify went against conventional wisdom:

- Free access acted as a marketing funnel

- Users experienced music without friction, competing directly with piracy

- Free listening normalized legal streaming before monetization

The freemium strategy was terrifying because every free user cost Spotify money upfront, yet it laid the groundwork for long-term subscriber growth (Wikipedia).

Freemium Worked — Only After Free Users Became Paying Users

Scaling proved the model:

- By 2018, 46% of users were premium subscribers, generating ~90% of revenue (Strategyzer).

- By 2025, 60% of premium users originated from the free tier (AInvest).

Spotify didn’t monetize music first. It monetized attention, habit, and time, then converted those into subscriptions.

Deep Insight: Monetizing Attention Over Content

The genius of Spotify’s freemium strategy was simple but radical:

- Hook users with free music

- Build habits with behavioral features

- Convert to premium with added convenience and fewer frustrations

By flipping traditional media monetization logic, Spotify turned a loss-making free base into a profitable subscription ecosystem. It was a strategy that required exceptional execution, patient investors, and a willingness to absorb losses for nearly a decade.

Chapter 4

Engineering the Product Around Constraints

This section is all about understanding how people actually use Spotify over time.

In this section, I’ll break down annual usage data from 2015 to 2025 and show you how listening habits, engagement levels, and user behaviour have evolved across the platform.

Most product stories focus on what users want.

Spotify’s story is different. Its evolution shows how technical limitations, costs, and business realities shaped every major feature long before user experience did. After securing licenses and committing to a freemium model, Spotify had to engineer a product that could survive those decisions. Every core functionality, from offline mode to shuffle limits, was born not to delight users, but to solve real constraints.

1. Bandwidth Limitations in Early Europe — The Invisible Constraint

In 2008–2009, Spotify launched across Europe (Sweden, Norway, Finland, Spain) into a world of slow mobile data and limited smartphone capabilities (engineering.atspotify.com).

Early devices and networks could barely stream music reliably. Spotify’s engineers faced hard infrastructure constraints, forcing them to optimize both data usage and power consumption. This wasn’t a UX preference. It was engineering survival. Without aggressive optimization, streaming simply would not have worked at scale in early mobile environments.

2. Offline Mode as a Survival Feature

Mobile networks were expensive, unreliable, and metered. Spotify needed a solution to make streaming viable. Offline mode became a premium feature that allowed users to download playlists and tracks (The Register).

Even today, the 10,000-track limit per device exists not arbitrarily, but to satisfy licensing and scalability rules (Spotify). Offline mode wasn’t “nice to have”. It was a structural workaround for infrastructure limits, especially in regions where mobile data costs were prohibitive.

3. Playlist Architecture as a Retention Engine

Playlists were engineered to replace ownership with habit. In a world where search alone wasn’t enough, user-generated playlists and curated collections became core retention mechanisms.

Engineers designed data structures for fast retrieval, syncing, and reordering across devices. Academic research shows playlists increase the psychological cost of leaving the service, turning time spent organizing music into a form of engagement (arXiv). What looked like personalization on the surface functioned as lock-in beneath it.

4. Shuffle, Skip Limits, and Ads — Product Decisions Rooted in Business Reality

Spotify’s free tier was a compromise between user freedom and label economics.

- Skip limits and shuffle mode were mandated by record labels to prevent free users from substituting piracy or premium subscriptions (Wikipedia).

- Free users could only stream on shuffle, skip a limited number of tracks, and hear ads.

- Ads subsidized royalty payouts for non-paying listeners, making the free tier financially sustainable.

Even in 2025, Spotify relaxed some shuffle restrictions once it had the scale and data to safely improve engagement without undermining premium incentives (Music Business Worldwide). Constraints eased only after Spotify earned the right to loosen them.

5. Why These “Constraints” Produced a Product That Worked

Spotify’s features weren’t designed for UX alone. They were solutions to real-world constraints:

- Offline mode solved connectivity and cost issues (engineering.atspotify.com).

- Playlist-centric design boosted engagement and habit formation (arXiv).

- Skip and shuffle limits enforced freemium economics (Wikipedia).

Together, these constraints produced a product that scaled efficiently, protected licensing relationships, and made Spotify increasingly difficult to replace. What began as limitation-driven engineering became a durable competitive advantage.

Chapter 5

The Algorithm Shift — When Discovery Replaced Search

This section looks at how Spotify’s product was engineered around the limits it couldn’t control.

I’ll break down the technical, licensing, and business constraints the team faced and show how those pressures shaped the product users actually experienced.

Spotify’s early product was search first. Users typed a song, artist, or album, and hit play.

By the mid-2010s, it became discovery first. Users opened Spotify not to find music, but to see what it had learned about them. This wasn’t accidental. It was the result of algorithmic personalization, built on behavior rather than explicit taste, crystallized in features like Discover Weekly. As Spotify’s catalog grew to tens of millions of tracks, search alone could no longer satisfy user needs; the product had to anticipate what listeners wanted before they asked.

Why Manual Curation Stopped Scaling

Before algorithms, music discovery relied on genre browsing, editor-curated playlists, and radio stations. But as Spotify’s catalog exploded into tens of millions of tracks, manual curation couldn’t keep up. Users couldn’t efficiently find new music worth their time.

Streaming services faced a structural problem: traditional search only solves “find this track,” not “find what you’ll like next.” Solving this required interpreting massive behavioral data and context signals (Digital Data Design Institute at Harvard).

Echo Nest Acquisition — A Strategic AI Foundation

On March 6, 2014, Spotify made a decisive move: acquiring The Echo Nest, a Boston-area music intelligence company focused on analyzing music characteristics and large-scale listening behavior (the.echonest.com).

Key points:

- Founded in 2005 out of MIT Media Lab, Echo Nest mapped tempo, timbre, semantic tags, and cultural data (Wikipedia).

- Spotify acquired it for roughly €49.7 million (~$68 million), primarily via equity (Grokipedia).

- Echo Nest became the core of Spotify’s “Taste Profiles,” translating listening behavior into predictive models for personalized recommendations.

This acquisition didn’t just improve recommendations; it fundamentally shifted Spotify’s product strategy from cataloging music to anticipating user preferences.

Birth of Discover Weekly — Personalization at Scale

July 2015: Discover Weekly launches. Every Monday, users receive a personalized playlist, dynamically generated using:

- Collaborative filtering — connecting users with similar listening histories.

- Content-based features — matching songs with similar acoustic or metadata attributes.

- Behavioral signals — learning from skips, playlist additions, and saves (Digital Data Design Institute at Harvard).

Its adoption was explosive: 40+ million users streamed over 5 billion tracks in the first year (dukespace.lib.duke.edu). Discover Weekly wasn’t just a playlist—it became a behavioral anchor, creating habitual, algorithm-driven engagement.

Training Users to Trust Algorithms

Discover Weekly transformed user experience by:

- Scheduled Anticipation — weekly delivery created a routine, turning discovery into habit (dukespace.lib.duke.edu).

- Behavior-Driven Precision — recommendations improved with each interaction, building trust (Digital Data Design Institute at Harvard).

- Personalization as a Feature — the product shifted from breadth to interaction depth, centering the experience around the individual.

Users stopped searching not because music was hard to find, but because the algorithm anticipated their preferences, changing behavior fundamentally. Personalization depended on user trust and reliable data, creating a feedback loop that reinforced engagement.

Trust, Security, and Data Integrity

In July 2020, cybersecurity researchers identified a large exposed database containing hundreds of millions of records linked to Spotify credentials, signalling an imminent credential-stuffing attack rather than a breach of Spotify’s internal systems. The data was traced to reused usernames and passwords harvested from earlier leaks across the internet, a common vulnerability at platform scale.

Spotify responded with a rolling password reset for affected accounts, emphasizing that personalization only works when users trust the system with their data. As recommendations became more intimate and behavior-driven, safeguarding access was no longer just a security function; it became foundational to the product itself.

Advanced Angle — Learning Behavior, Not Predicting Taste

Spotify’s discovery engine doesn’t guess your favorite song—it learns it:

- Tracks you listen to and skip

- Songs you save or replay

- Patterns aligning with millions of other users

These feed into a “taste vector,” evolving with every interaction. Over time, Spotify becomes less about explicit requests and more about implicit enjoyment. Internal testing confirmed the accuracy: employees reported that recommendations felt like a “secret music twin” curated their playlists (IEEE Spectrum), highlighting the power of behavioral modeling.

Chapter 6

Growth Without Hardware — Beating Apple at Its Own Game

This section explores how Spotify grew massively without selling any hardware of its own.

I’ll break down the strategies, partnerships, and platform moves that let it compete with Apple and capture listeners worldwide.

Spotify’s growth advantage wasn’t better music.

It wasn’t better branding.

And it definitely wasn’t deeper pockets.

It was something far more structural.

Spotify never tried to own the device.

It tried to exist on every device.

That single decision explains how Spotify could compete with Apple, a company that controls the world’s most powerful hardware ecosystem, without manufacturing a single piece of hardware itself.

Why Spotify Avoided Hardware Dependency (By Design)

From the beginning, Spotify positioned itself as a software-first platform, not a device-anchored service.

Early investor materials and later SEC filings make this explicit: Spotify viewed hardware ownership as a distribution bottleneck, not a competitive advantage.

In its 2018 F-1 filing (PDF) Spotify states that its growth strategy depended on:

“Broad platform availability across operating systems, devices, and form factors”

—not on exclusive ecosystems.

That distinction mattered because hardware ecosystems impose hard constraints:

- Slower global rollout

- High capital expenditure

- Platform lock-in that limits reach

Apple Music, launched in June 2015, followed a vertical strategy:

iPhone → iOS → Apple Music

Spotify chose the opposite path:

Device-agnostic first. Ecosystem-agnostic always.

Deep Integrations: Winning Inside Other People’s Ecosystems

Rather than fighting platforms, Spotify embedded itself inside them.

Apple iOS (Yes — Even Apple’s Platform)

Despite competing directly with Apple Music, Spotify remained one of the most downloaded apps on iOS.

By 2014, it ranked among the top music apps on Apple’s App Store across Europe and the U.S. (Statista report).

After Apple Music launched in 2015, Spotify continued operating natively on iOS, accepting Apple’s 30% App Store fee as a distribution cost, not a fatal disadvantage.

This was a deliberate trade-off: reach over margin, a priority Spotify has repeatedly reinforced in shareholder communications.

Android: Default, Not Optional

Spotify launched on Android in April 2009, making it one of the earliest premium streaming apps on the platform.

By 2013, Android accounted for a majority of Spotify’s mobile listening hours globally (Spotify Engineering Blog).

This gave Spotify immediate scale in markets where iPhones were not dominant, especially across Europe, Latin America, and later India.

Consoles & Living Rooms

In 2015, Spotify launched on PlayStation 3 and 4, integrating directly into Sony’s console ecosystem.

Sony later confirmed that Spotify replaced its own Music Unlimited service, effectively outsourcing music streaming across millions of consoles (Sony press release).

Why this mattered:

- Console users skew younger

- Listening sessions are long

- Music becomes ambient, not intentional

Spotify wasn’t just an app anymore; it became background infrastructure.

Cars: Distribution Where Habits Are Locked In

Spotify’s automotive integrations began as early as 2013, with partnerships spanning Volvo, Ford, BMW, and later Apple CarPlay and Android Auto.

According to Spotify’s 2019 Annual Report (PDF), automotive listening became one of the fastest-growing use cases, driven by commuting, a daily and repeated behavior.

Facebook Virality Phase (2011–2013)

One of Spotify’s most explosive growth moments came from Facebook integration.

In September 2011, Spotify launched frictionless sharing via Facebook’s Open Graph. Songs played on Spotify appeared directly in users’ feeds—turning listening into a social signal.

The result:

- Over 10 million new users in under a year

- U.S. users tripled between 2011 and 2012

This wasn’t advertising; it was distribution through behavior. Spotify didn’t buy users. Users broadcasted Spotify for free.

Carrier Bundling: Turning Telecoms Into Sales Teams

Spotify’s most underestimated growth lever was carrier bundling.

Early Europe (2009–2012)

Spotify partnered with TeliaSonera in Sweden and Finland, bundling Spotify Premium with mobile plans.

To users, Spotify felt “free.” In reality, carriers paid Spotify per subscriber.

According to the TeliaSonera bundled music services executive summary (PDF), bundled users showed:

- Lower churn

- Higher data usage

- Higher ARPU

Spotify quickly replicated this model across Europe.

Global Expansion (2013–2018)

Spotify later signed bundling agreements with Vodafone, AT&T, Orange, and Deutsche Telekom.

By 2018, Spotify disclosed that a material portion of Premium subscribers originated through bundled partnerships (F-1 filing PDF).

This strategy allowed Spotify to:

- Reduce direct CAC

- Enter new markets faster

- Leverage telecom billing infrastructure

Once again: no hardware, no retail stores, no logistics.

Strategic Insight: Horizontal vs Vertical Growth

- Apple grew vertically: Hardware → OS → Services → Margin control

- Spotify grew horizontally: Every device → Every OS → Every context → Maximum reach

Apple optimized for profit per user.

Spotify optimized for users per platform.

In a market defined by habit, repetition, and daily use, reach mattered more than ownership. Spotify’s device-agnostic strategy allowed it to scale globally faster, build massive engagement, and stay competitive against companies with vastly deeper pockets.

Chapter 7

The Economics of Streaming (Why Spotify Isn’t as Profitable as You Think)

This section dives into the economics behind Spotify and why high usage doesn’t equal huge profits.

I’ll break down revenue, costs, and the financial pressures of streaming to show why the platform’s growth often outpaces its profitability.

Spotify is the world’s largest music streaming platform.

Yet for most of its existence, it didn’t produce sustainable profits, even as usage exploded.

To understand why, you can’t look at users, streams, or downloads.

You have to follow the money.

Spotify’s business model creates massive scale, but its economics are governed by four structural realities:

- How revenue is split

- How royalties are calculated

- Why per-stream payouts feel low

- Why geography (ARPU) matters more than people think

Once you understand these mechanics, Spotify’s long road to profitability stops looking like failure, and starts looking structural.

Revenue Split Anatomy — Who Actually Gets Paid

Spotify doesn’t keep most of the money it earns.

According to industry reporting and Spotify’s own disclosures (Spotify Annual Report 2024), the company historically pays around 70% of total revenue to rights holders, including record labels, publishers, and collecting societies.

That single fact defines the business.

In practice:

- ~70–74% of revenue goes to content licensing and royalties

- ~26–30% remains for everything else: infrastructure, R&D, marketing, and operations

After cloud costs, engineering salaries, and growth spend, very little remains for traditional operating profit.

This is fundamentally different from SaaS or cloud platforms, where marginal usage is cheap.

For Spotify, usage itself is the cost.

The Per-Stream Payout Myth

One of the biggest misconceptions in streaming is the idea of a fixed payout per stream, numbers like “$0.003 per play.”

That’s not how Spotify works. It uses a pro-rata revenue-share model:

- All subscription and ad revenue is pooled

- Roughly 70% goes to rights holders

- Each track earns a share based on its percentage of total streams

If a song represents 5% of total platform streams in a month, it receives about 5% of the royalty pool. There is no fixed per-stream rate.

What people quote as “per-stream payouts” are emergent averages, not contractual guarantees.

Industry estimates typically place Spotify’s average payout around $4,000 per million streams, but that number varies dramatically based on:

- Premium vs ad-supported listeners

- Country and regional ARPU

- Individual licensing agreements

This is why the same song can earn wildly different amounts depending on who streams it and where.

Why Margins Stay Thin — Streaming Is a Variable-Cost Business

Most digital companies benefit from operational leverage: once software is built, additional users cost very little.

Spotify doesn’t.

Its largest expense — music licensing — scales directly with usage:

- More streams → higher royalty payouts

- More subscribers → more revenue, but also more obligations

- More free users → ad revenue, but still royalties

Even after fixed costs like engineering, marketing, and infrastructure, the core issue is structural: primary cost scales with the primary revenue driver. This explains why Spotify’s margins remained narrow for most of its history, even as revenue surged.

ARPU Is Destiny — Geography Shapes Profitability

Spotify’s average revenue per user is not global — it’s geographic.

- North America and Western Europe generate high ARPU due to pricing power

- Emerging markets (India, Southeast Asia, parts of Latin America) generate lower ARPU due to local pricing and weaker ad markets

This creates two effects:

- High-ARPU users subsidize low-ARPU users

- Global scale boosts revenue faster than margins — unless ARPU rises

This is why Spotify’s margin expansion coincided with subscription price increases in mature markets, especially in 2023–2024.

More users alone don’t fix the economics.

Better ARPU does.

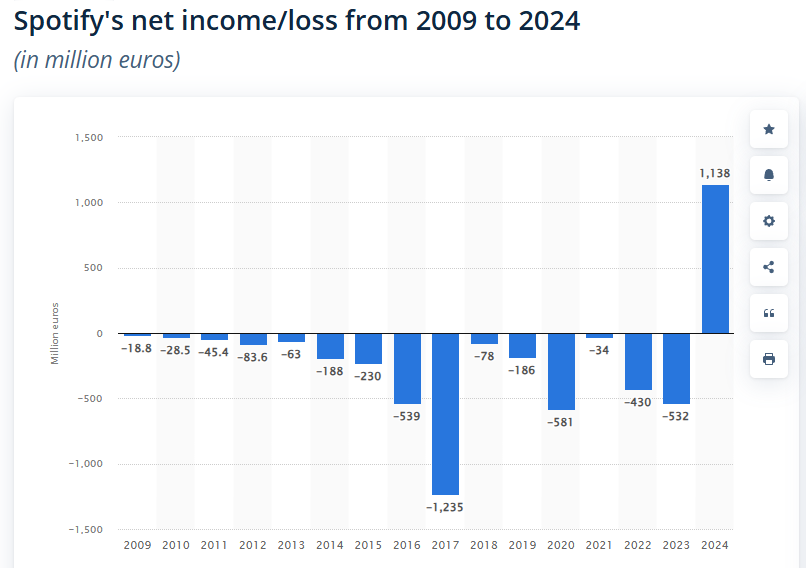

The Long Path to Profitability

Spotify didn’t flip a switch and become profitable.

It pulled multiple levers — slowly.

- Premium Dominance: By 2025, Premium subscriptions accounted for ~88% of total revenue, with ads contributing roughly 12%.

- Gross Margin Expansion: Gross margins climbed past 30%, driven by pricing changes, cost discipline, and revenue mix improvements.

- First Annual Net Profit: In 2024, Spotify reported its first full-year net profit — approximately €1.1 billion on €15.6 billion in revenue.

That milestone came after nearly two decades of structural optimization — not short-term tweaks.

Why Spotify’s Model Still Works (Even With Thin Margins)

At first glance, Spotify looks like a low-margin business.

In reality, it works because of scale, not because of unit economics.

- Scale drives revenue, even when costs scale too

- Global diversification stabilizes income

- Licensing scale creates a moat competitors struggle to cross

- Non-music content (podcasts, audiobooks) improves margins

- Revenue-share payouts expand when ARPU grows faster than costs

Spotify doesn’t monetize music the way traditional media did.

It monetizes engagement at scale.

Bottom Line: Streaming Economics Are Different

Spotify’s business model is unusual — and often misunderstood:

- 70%+ of revenue goes to rights holders

- Per-stream payouts are not fixed

- Margins depend on geography and ARPU mix

- Profitability required years of scale and pricing power

Spotify didn’t fail to profit early.

It paid the cost of building global infrastructure first — then optimized the economics. That’s why its profitability wasn’t quick.

And that’s why it was inevitable.

Chapter 8

Artists vs Spotify — A Relationship Under Constant Tension

This section explores the ongoing tension between artists and Spotify and what it means for music on the platform.

I’ll break down conflicts, revenue issues, and creative debates to show how this relationship has shaped both the company and its users.

Spotify’s 2024 Loud & Clear report revealed that the platform paid over $10 billion in music royalties — the largest annual payout in industry history. That sum accounted for more than 60 % of the company’s €15.7 billion revenue for the year.

Over the past decade, Spotify’s annual payouts have grown roughly 10× — from about $1 billion in 2014 to over $10 billion in 2024 — reflecting how streaming revenue scaled alongside global adoption.

Spotify also highlighted that in 2024:

- Nearly 1,500 artists earned over $1 million in royalties from Spotify alone. (Digital Music News)

- Independent artists and labels collectively generated more than $5 billion, roughly half of total Spotify royalties. (Loud and Clear)

Taken together, these figures show that Spotify’s total economic impact on recorded music is enormous — larger than any single retailer during the peak of the CD era. (Loud and Clear)

Yet beneath these impressive headline numbers lies a very different reality for the majority of creators.

Despite record payouts, most artists still earn very little from streaming. Industry data shows that only a small fraction of artists generate meaningful income through Spotify royalties — even in 2024. For example, only 0.6 % of artists earned at least $10,000 in royalties on the platform last year. (Music Business Worldwide)

This uneven distribution reflects the pro‑rata royalty model discussed in Chapter 7, where payouts are based on each artist’s share of total streams rather than a fixed per‑stream rate (see Spotify’s royalties explanation).

Because royalties are allocated proportionally, a small number of top artists capture a disproportionate share of revenue, while the vast majority earn modest amounts. Geography, subscription type, listener behavior, and contractual deals with labels further influence earnings, creating a highly skewed income landscape. These contrasting realities — enormous total payouts versus highly unequal earnings — lie at the heart of ongoing debates over Spotify’s royalty model and how streaming income is distributed in the music industry.

Chapter 9

Podcasts, Exclusivity, and the Platform Pivot

This section is all about understanding how people actually use Spotify over time.

In this section, I’ll break down annual usage data from 2015 to 2025 and show you how listening habits, engagement levels, and user behaviour have evolved across the platform.

Spotify’s early success with music streaming gave it scale. But by the late 2010s, the company began looking for growth engines beyond music — and identified podcasting as a strategic opportunity. At a deeper level, Spotify’s move into podcasts wasn’t really just about audio formats. It was about diversifying revenue, owning more of the listening experience, and reducing dependence on music royalties.

Why Music Alone Wasn’t Enough

By the mid‑2010s, Spotify’s core music business was growing fast, but its economics remained constrained by high royalty costs and thin margins.

Podcasts offered several structural advantages:

- Lower content costs — most podcasts do not require per‑play royalties to music labels or publishers

- Higher ad monetization — long‑form podcast ads often command higher CPMs

- Habit expansion — podcasts increase session length and listening frequency

These dynamics made podcasting a natural extension of Spotify’s platform — capable of driving both engagement and monetization in ways music alone could not. (Digital Music News, 2020)

The Joe Rogan Deal — A Flagship Investment

One of the most visible moves in Spotify’s podcast push was its exclusive deal with The Joe Rogan Experience. In 2020, Spotify signed Rogan to a multi‑year exclusive licensing agreement worth an estimated hundreds of millions of dollars, bringing one of the most listened‑to podcasts exclusively onto its platform to drive user acquisition and differentiation. (Spotify Newsroom)

By 2025, Spotify renewed Rogan’s contract with a major shift — the show became non-exclusive, expanding distribution to platforms like Apple Podcasts, Amazon, and YouTube while Spotify retained control over advertising. This agreement was reportedly valued at up to $250 million, reflecting a pivot toward broader monetization rather than strict exclusivity. (PodcastVideos.com)

This strategic change signaled a broader realization: reach and ad revenue can outweigh exclusivity when building scale, especially in a category where advertiser dollars — not incremental subscriptions — often drive profitability.

Anchor and the Podcast Stack — Tools Over Ownership

Spotify’s podcast strategy wasn’t limited to signing individual shows. It also focused on owning the infrastructure layer of podcast creation and monetization:

- In 2019, Spotify acquired Gimlet Media, a narrative podcast network, for a reported ~$230 million.

- In the same year, Spotify acquired Anchor, a podcast creation and hosting platform, lowering the barrier for creators to publish directly on its ecosystem.

- Also in 2019–2020, Spotify acquired Parcast, a scripted podcast network, expanding genre diversity and content depth.

- In 2020, it acquired Megaphone, a leading podcast advertising platform, to strengthen monetization infrastructure.

Together, these acquisitions gave Spotify end‑to‑end control: from creation and publishing to analytics and ad monetization, positioning it as a creator platform as well as a distribution hub.

The Bigger Picture

Spotify’s podcast journey reflects a broader platform pivot: from hosting music to becoming an audio ecosystem that supports creators, engages listeners across formats, and drives diversified revenue through ads, subscriptions, and tools.By focusing on infrastructure, analytics, and monetization rather than exclusivity, Spotify ensured that the platform could scale with engagement and advertising potential. This pivot demonstrates that platform growth often depends more on reach and engagement than on owning content alone. (Spotify Newsroom, 2023)

Chapter 10

Spotify vs Its Rivals — Strategic Differences, Not Features

This section looks at how Spotify sets itself apart from competitors through strategy, not just features.

I’ll break down the approaches, partnerships, and decisions that let Spotify outperform rivals and shape user experience over time.

By 2025, Spotify faces competition on nearly every front: Apple Music, YouTube Music, and Amazon Music are all major players in the streaming audio space. At first glance, the battle might appear to be about catalog size, interface, or exclusive content. But the real difference is far deeper: it’s about ecosystem strategy, distribution philosophy, and user habit formation.

Platform Comparison: Music Streaming Services (2025)

| Platform | Catalog (approx.) | Paid Subscribers | Notes |

| Spotify | 100+ million | 230M+ | Freemium + ad-supported model drives trial and habit |

| Apple Music | 100+ million | 105M+ | No free tier, deep OS integration (iOS/macOS) |

| YouTube Music | 100+ million | 50M+ | Leverages YouTube’s massive video+audio ecosystem |

| Amazon Music | 100+ million | 50M+ | Bundled with Prime, less social/playlist focus |

The catalog difference is minimal. So why does Spotify lead in habit and engagement? The answer lies in product strategy and distribution philosophy.

Ecosystem vs Algorithm

Apple Music relies heavily on tight OS integration. Its growth is tied to iPhone adoption and legacy iTunes users. This approach locks users inside the Apple ecosystem, driving adoption among iOS loyalists — but limiting cross-platform virality and habit portability.

Spotify, in contrast, is platform-agnostic. Its core advantage lies in:

- Algorithm-driven playlists such as Discover Weekly, Daily Mix, and Release Radar, which train users to trust Spotify for discovery

- Cross-platform availability — iOS, Android, desktop, consoles, smart TVs, and smart speakers

- Freemium access — instant trial without commitment

This explains why Spotify doesn’t need OS control to win. It wins by shaping listening habits, not enforcing ecosystem lock-in. Its strategy emphasizes user engagement, personalized discovery, and frictionless access, creating a competitive moat that rivals relying on hardware, ecosystem, or bundling cannot easily replicate.

YouTube Music and Amazon Music rely on existing user bases and bundled services, respectively, rather than habit-driven discovery. While these platforms benefit from integration into larger ecosystems (Google and Amazon), their algorithmic personalization and habit formation mechanisms are less central than Spotify’s, which remains the platform’s most enduring advantage.

Chapter 11

Strategic Lessons From Spotify’s History

This section is all about understanding how people actually use Spotify over time.

In this section, I’ll break down annual usage data from 2015 to 2025 and show you how listening habits, engagement levels, and user behaviour have evolved across the platform.

After spending weeks diving deep into Spotify’s journey, one thing became crystal clear: this isn’t just a story about music. It’s a masterclass in strategy, product design, and growth. And the lessons are gold for anyone building a business or product today.

Solve the Right Problem, Not the Obvious One

When I first looked at Spotify, I thought: “It’s just another music app.”

But the more I researched, the more I realized they weren’t selling music. They were solving piracy and friction.

Instant streaming. Massive catalogs. No ownership headaches. That’s the real magic.

Most startups focus on features. Spotify focused on the problem no one else could solve.

Lesson for me? Always ask: what problem am I truly solving?

Constraints Are Secret Superpowers

Licensing, bandwidth, freemium economics—Spotify had constraints everywhere.

But here’s the kicker: every constraint shaped a feature that worked.

Offline mode? Born from data limits.

Skip limits? Born from licensing rules.

Playlists? Engineered to hook users and keep them coming back.

After studying this, I realized constraints aren’t barriers—they’re innovation fuel.

Growth Without Owning Anything

Spotify never tried to make a phone or a speaker. It didn’t need to.

Instead, it went everywhere: iOS, Android, consoles, cars, smart TVs.

Freemium pulled users in. Carriers and social integration spread it like wildfire.

I learned something huge here: reach beats ownership. Always.

Monetize Attention, Not Content

Here’s a truth most people miss: Spotify didn’t make music profitable—they made attention profitable.

Free users became paying users. Podcasts added ad revenue. Recommendations turned habit into subscription.

Every insight from my research screamed: monetize behavior, not the product itself.

Patience is a Strategy

Spotify lost money for years. Yet every move—from label equity deals to global expansion—was calculated.

They aligned incentives with partners. Took risks. Waited. Scaled.

That hit me hard: long-term strategy wins over short-term thinking every time.

Personalization Creates Moats

Discover Weekly, Daily Mix, Release Radar—these aren’t just playlists.

They’re behavioral magnets. Spotify learned users’ habits before the users even realized it.

And that’s how a company without hardware beat Apple, Amazon, and YouTube.

Lesson? Build experiences so sticky, users can’t imagine leaving.

My Takeaway

After all this research, I’m convinced: Spotify’s playbook is universal.

Solve real problems.

Turn constraints into advantages.

Scale horizontally, not vertically.

Monetize behavior, not content.

Invest patience into strategy.

And always, always build habit-forming experiences.

Spotify didn’t just change music. It rewrote the rules for modern platforms.And now, after analyzing every chapter, every pivot, and every lesson, I know one thing for sure: these strategies aren’t just for music—they’re for any business that wants to dominate its market.